Jun 2025

Choosing the right payment apps for personal and professional use can be daunting when faced with so many options for similar purposes. Here are a few suggestions for the best apps for payment by category, updated for 2025. Whether you need a convenient way to pay back friends for dinner, a digitally enhanced in-store solution, or a hassle-free way to send money overseas, one of these payment apps will have you covered.

Before diving into our reviews, here's a quick overview of the main types:

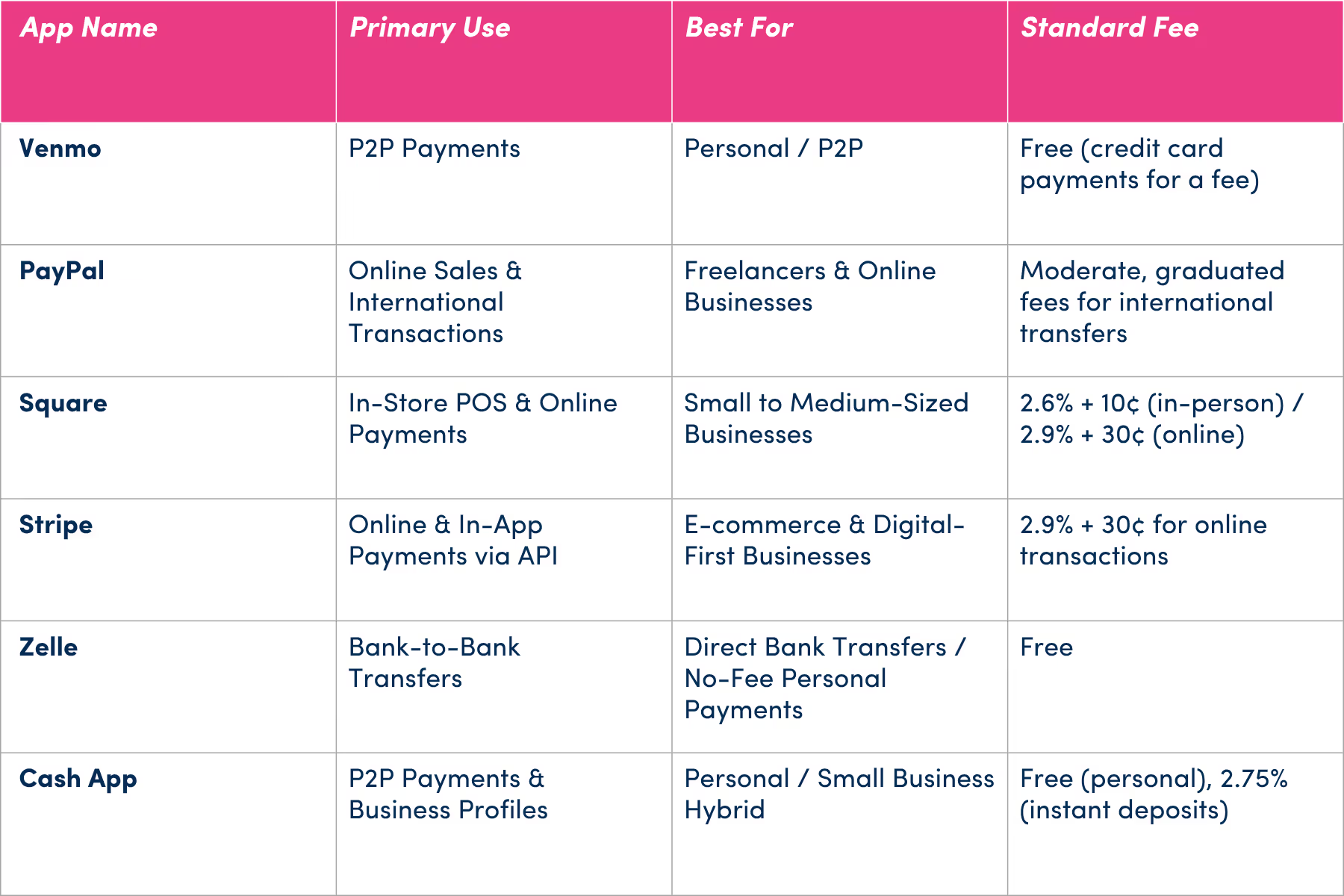

Venmo quickly became synonymous with P2P payments, such as splitting bills with friends, paying roommates for rent, or casual reimbursements. You can send and receive money to and from other Venmo users after linking a bank account, credit card, or debit card.

Venmo’s social element allows users to add friends, which speeds up future payments and helps confirm that money is being sent to the right person. You can also set privacy options to control who sees your transaction history. Venmo now offers a Venmo debit card—and supports credit card payments for a fee.

Venmo’s success isn’t just about payments—it’s about making finance social and frictionless. The social feed allows users to show (at a high level) what or where they made a purchase, creating organic marketing opportunities. For businesses building fintech apps, this proves that reducing friction and adding social elements can drive massive user adoption. More than 50% of Venmo users are Millennial and Gen Z, showing the importance of designing for younger demographics.

Cash App (formerly Square Cash) is similar to Venmo in that it’s primarily a peer-to-peer payment app. Like Venmo, Cash App has business profiles that allow businesses to accept payments directly through the app. This is particularly useful for online businesses or those that want to offer a convenient payment option for customers who already use Cash App.

Cash App also can work seamlessly with Square hardware, allowing businesses to accept in-person payments using physical card readers. This makes it a more versatile option for businesses that need both online and in-person payment processing. Cash App combines the convenience of a peer-to-peer payment app with the functionality of a traditional point-of-sale system, making it a good choice for businesses that need both.

Cash App also can work seamlessly with Square hardware, allowing businesses to accept in-person payments using physical card readers. This integration between consumer and business products creates a powerful ecosystem. Cash App’s success in adding features like stock trading and Bitcoin shows how payment apps can become financial super-apps. The lesson: once you have user trust and daily engagement, you can expand into adjacent financial services.

Zelle differs slightly in that it is integrated with many banks and credit unions, allowing users to send money directly between bank accounts in minutes without needing a separate app. It’s a simple, secure, and fee-free option for those who prefer a direct connection to their bank. Unlike Venmo and Cash App, Zelle does not have social features but is ideal for fast, no-hassle bank transfers using an email address or phone number.

Zelle is integrated into many US bank apps, enabling instant bank-to-bank transfers without needing additional apps. This shows the power of leveraging existing infrastructure rather than competing with it. For fintech startups, partnering with established institutions can provide instant credibility and distribution that would take years to build independently.

For more than two decades, PayPal has been driving the world of online payments. It allows users to send and receive cash transfers from countless countries outside the US for moderate, graduated fees. Likewise, PayPal is an ideal option for international purposes as users can switch between currencies and use more than just US dollars. The one catch is that both the sender and receiver must have a PayPal account.

PayPal’s 20+ year dominance demonstrates the power of being first and building trust at scale. Their evolution from simple online payments to a comprehensive financial ecosystem shows how successful fintech companies must continually innovate. For businesses developing payment solutions, PayPal’s extensive API documentation and global reach set the standard for what enterprise clients expect.

Square began as a mobile card reader but has grown into a comprehensive business solution. A point of sale (POS) system is a hardware and software solution used for in-store payments. Square now offers in-person and online payment processing, a free POS app, basic hardware, and inventory management. Square integrates with third-party apps for marketing, payroll, and appointment scheduling, making it an excellent choice for small to medium-sized businesses.

Square’s journey from a simple mobile card reader to a full business ecosystem exemplifies the power of solving one problem exceptionally well, then expanding. They identified that small businesses needed affordable, accessible payment processing and built from there. This iterative approach—start simple, listen to users, expand strategically—is a blueprint to follow when developing fintech solutions for digital products.

Stripe is known for its powerful API, enabling businesses to create scalable payment solutions that can handle rapid growth. Businesses can accept payments from various sources, such as credit cards, debit cards, and digital wallets. Stripe is also highly customizable, making it a popular choice for digital-first businesses that want to tailor the payment experience to match their brand and preferences.

While Stripe is primarily a software-based solution, it can be used with physical card readers, allowing businesses to accept in-person payments. It doesn’t require a specific reader and is compatible with many options on the market.

Stripe’s success in the business-to-business market is built on its powerful and flexible API, which allows developers to create highly customizable and scalable payment solutions. This focus on a seamless developer experience makes Stripe a top choice for e-commerce and digital-first businesses that want to tailor the payment process to their specific brand and needs. By empowering companies to handle rapid growth and accept various payment methods like credit cards, debit cards, and digital wallets through this robust integration, Stripe proves that a superior developer experience is key to winning the B2B market.

Apple Pay, an early leader in the digital wallet space, continues to dominate contactless payments. Apple Pay features broad support for online shopping and in-app purchases, making it a versatile option for those seeking both convenience and security. Additionally, Apple Pay works seamlessly with Apple Watch and other iOS devices, making it a go-to choice for iPhone users.

Apple Pay’s seamless integration across the Apple ecosystem demonstrates the competitive advantage of platform lock-in done right. They made payments invisible—just double-click and authenticate. For businesses building payment solutions, the lesson is clear: the best payment experience is one the user barely notices. Focus on reducing steps, not adding features.

Google Wallet (formerly Google Pay) offers a comprehensive payment experience, allowing users to complete both physical and virtual transactions. Google Wallet is only supported on Android devices. Like Apple Pay, Google Wallet supports contactless payments, in-app purchases, online shopping, and more beyond digital payments as well.

Google Wallet’s evolution (from Google Checkout to Google Pay to Google Wallet) shows that even tech giants must pivot when user adoption lags. Their current success comes from finally matching Apple’s simplicity while adding unique features like loyalty card storage. This resilience and willingness to rebuild is essential in fintech, where user trust is hard-won and easily lost.

Xoom, a PayPal-owned service, lets users skip the account and still send and receive money internationally. Xoom relies on a more case-based fee system that depends on the type of payment source (like a credit card or a bank account) as well as the country. With this setup, certain international transactions—especially when using a credit card—can require high fees, while others are free. Xoom can be used to send money, top up prepaid mobile phones, and pay bills globally if you reside in the US, Canada, the UK, and most countries within the European Economic Area.

Xoom’s focus on international remittances proves the value of solving a specific pain point for an underserved market. Rather than competing broadly, they excel at cross-border transfers with transparent fees and multiple payout options. For fintech developers, this targeted approach—finding a specific problem and becoming the best solution—often beats trying to be everything to everyone.

While the payment apps on this list excel at their intended purposes, growing businesses often hit limitations that require custom solutions. Here’s when it's time to consider building your own payment infrastructure:

Outside of the scenarios mentioned here, Venmo may not otherwise be used to receive business, commercial, or merchant transactions, meaning you can’t use Venmo to accept payment from (or send payment to) another user for a goods or services, unless explicitly authorized by Venmo. Using personal payment apps for business isn’t just risky—it can result in frozen accounts and lost revenue.

Compliance Nightmares: As transaction volumes grow, you’ll face increasing regulatory scrutiny. Consumer apps aren’t designed for complex tax reporting, PCI compliance, or industry-specific regulations like HIPAA for healthcare payments.

Integration Limitations: Need to connect payments to your inventory system? Want automated reconciliation with your accounting software? Most consumer apps offer limited or no API access for custom integrations.

Brand Dilution: Sending customers to third-party apps breaks your brand experience. You lose control over the checkout flow, can’t customize the interface, and miss opportunities to upsell or cross-sell.

Data Blindness: Consumer apps provide basic transaction data, but lack the deep analytics businesses need. You can’t track customer lifetime value, segment payment behaviors, or identify fraud patterns.

Building a tailored payment solution isn’t just about avoiding limitations—it’s about creating competitive advantages. Custom solutions can reduce transaction fees, increase conversion rates, and provide the exact features your business model demands. Most importantly, you own the entire customer experience and data.

The success of these apps proves the immense opportunity in fintech. From seamless P2P payments to innovative business solutions, the right app can transform an industry. If you have an idea for a fintech solution, our team has the expertise to navigate the complexities of financial app development. Let’s build the next app on this list together.

Have an idea? We help clients bring ideas to life through custom apps for phones, tablets, wearables, and other smart devices.

Work with usWe help brands thrive in the digital world.

Inspired Where We Are—Our team of experts is 100% US-based, delivering user-inspired digital products from Boulder and beyond.